Metal Recycling Market Size to Worth USD 1,071.11 Billion by 2034

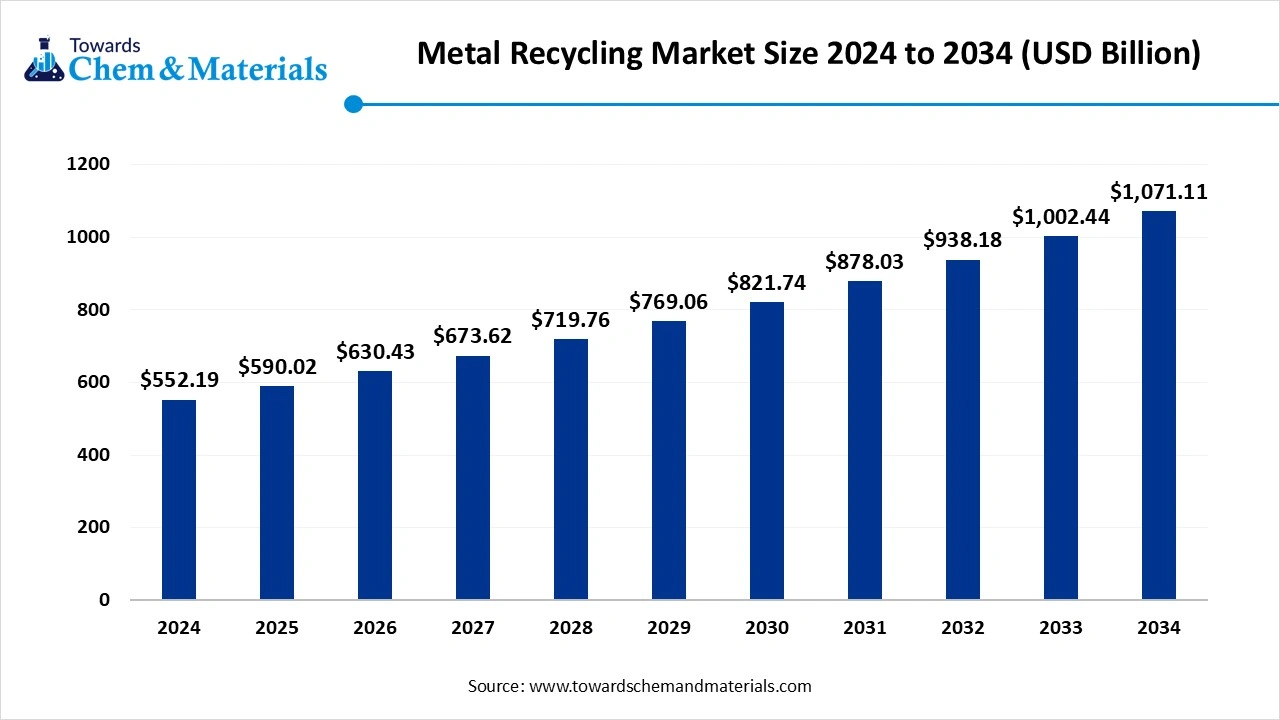

According to Towards Chemical and Materials, the global metal recycling market size is calculated at USD 590.02 billion in 2025 and is expected to be worth around USD 1,071.11 billion by 2034, growing at a compound annual growth rate (CAGR) of 6.85% over the forecast period 2025 to 2034.

Ottawa, Oct. 07, 2025 (GLOBE NEWSWIRE) -- The global metal recycling market size was valued at USD 552.19 billion in 2024 and is anticipated to reach around USD 1,071.11 billion by 2034, growing at a compound annual growth rate (CAGR) of 6.85% over the forecast period from 2025 to 2034. A study published by Towards Chemical and Materials a sister firm of Precedence Research.

Download a Sample Report Here@ https://www.towardschemandmaterials.com/download-sample/5830

Metal Recycling Overview

The Rising demand for sustainable raw materials is driving growth in the market. the global metal recycling market operates on the principal of reclaiming metals from discarded goods and industrial waste and reintroducing them into manufacturing cycles, reducing dependency on virgin ores while supporting environmental and economic sustainability. It is driven by rising industrialisation, growing demand for metals in sectors like construction, automotive, and electronics, and increasing regulatory pressure to reduce carbon footprints and landfill waste. Advanced sorting and processing technologies, such as shredding, separation, and refining, are becoming more integral to improving recovery efficiency. The Asia Pacific region holds substantial influence consumption. In the coming years, the market is expected to expand steadily as metal demand continues to rise, technology evolves, and stakeholders increasingly adopt circular economy practices.

Metal Recycling Market Report Highlights

- The Asia Pacific metal recycling market size was estimated at USD 248.49 billion in 2024 and is expected to hit around USD 482.64 billion by 2034, growing at a compound annual growth rate (CAGR) of 6.86% over the forecast period from 2025 to 2034.

- By region, Asia Pacific held approximately a 45% share in the metal recycling market in 2024 due to the growing industrial activities.

- By metal type, the ferrous metals segment held approximately a 65% share in the market in 2024 due to the growing use of steel & iron in various industrial applications.

- By scrap source, the industrial scrap segment held approximately a 50% share in the market in 2024 due to the growing manufacturing sector.

- By processing method, the melting & refining segment held approximately a 40% share in the market in 2024 due to the growing demand for high-quality metals.

- By end-use industry, the construction & infrastructure segment held approximately a 45% share in the market in 2024 due to the growing construction activities.

Buy Now this Premium Research Report at a Special Price Against the List Price With [Express Delivery] @ https://www.towardschemandmaterials.com/price/5830

Metal Recycling Market Report Scope

| Report Attribute | Details |

| Market size value in 2026 | USD 630.43 billion |

| Revenue forecast in 2034 | USD 1,071.11 billion |

| Growth rate | CAGR of 6.85% from 2025 to 2034 |

| Actual data | 2020 - 2024 |

| Forecast period | 2025 - 2034 |

| Quantitative units | Revenue in USD billion, volume in million tons, and CAGR from 2025 to 2035 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments covered | Metal, Scrap Source, Processing Method, End-Use Industry, region |

| Key companies profiled | CMC; European Metal Recycling; Novelis; Norsk Hydro ASA; Tata Steel; GFG Alliance; Kimmel Scrap Iron & Metal Co., Inc; Schnitzer Steel Industries, Inc., Sims Metal, Utah Metal Works |

For more information, visit the Towards Chemical and Materials website or email the team at sales@towardschemandmaterials.com| +1 804 441 9344

Why Is It Important to Recycle Metals Market?

1. To preserve natural resources. Recycling metal replaces the need to produce virgin metal. In turn, this preserves precious natural resources like coal and iron ore used in metal production. It’s essential to consider resources like coal, as its combustion is a top contributor to climate change. In 2010, coal accounted for 43% of global greenhouse gas emissions and this climate issue has perpetuated ever since. As it simultaneously uses less energy and cuts down on using natural resources, recycling metals is an environmental activity — and an easy way to take corporate responsibility.

2. To best use raw materials. Metals are amongst the few raw materials easily recycled without damaging their original properties. This means there isn’t any real reason to create new metal — apart from to meet increased demand. The recycling process can be repeated as many times as needed, even with valuable metals such as aluminium.

The list of recyclable metals is extensive, with only radioactive metals (uranium, plutonium) and toxic metals such as lead and mercury prohibited. There aren’t many disadvantages to recycling metals, but a total waste management company can help you deal with any issues. Scrap metal recycling facilities will always accept a wide range of metals like steel, as operators know the value of metal won’t decrease.

3. To offset your business’s carbon emissions. There’s an increasing emphasis on companies recycling all raw materials to achieve ambitious “zero to landfill” targets. Recycling metals is an environmental alternative to other forms of disposal, as it cuts down emissions and reduces air pollution. By recycling metals, you’re contributing to your business’s carbon goals. Above all, the recycling process will help eliminate pollution from the atmosphere and encourage others to make the most of metal’s versatile usage.

A tonne of aluminium recycled saves nine tonnes of CO2 emissions from being released into the atmosphere. The Planet Mark environmental foundation confirms that every tonne of aluminium recycled conserves five tonnes of bauxite — the raw material from which aluminium is made.

4. To save money by reducing production costs. Recycling metals offers financial incentives and there’s no shame in benefiting from these. Most companies recycle on the basis that it’s cheaper to do so, allowing you to drive down production costs (and convert this spend into collection costs). It’s much more affordable to use existing waste metal than to create it from scratch.

5. To meet recycling industry standards. As people grow more concerned about the environment, the recycling industry is putting additional pressure on businesses to recycle. Companies are expected to recycle materials where possible, with metal recycling being a huge part of this. Needless to say, if you have scrap metal lying around on-site, you should take action. You’re also benefiting the economy by recycling metals as the recycling industry provides employment in waste facilities.

Metal recycling means raw material security and environmental protection

Europe has a high copper demand but limited natural resources. Metal recycling opens up the metal reserves found in products and therefore makes a considerable contribution to the supply of copper and other metals.

Copper recycling fulfills the criteria for sustainable development and is the foundation of modern recycling management. It conserves natural resources, reduces energy demand and prevents the loss of valuable materials.

Most non-ferrous metals and precious metals have outstanding recovery properties. Recycling copper, silver, gold and other non-ferrous metals doesn’t lead to losses of quality in the metals and can be repeated as often as desired.

What Are the Major Trends in the Metal Recycling Market?

- Growing emphasis on sustainability and circular economy models is pushing industry players to integrate recycled metals more deeply into supply chains.

- Increasing adoption of advanced sorting, shredding, and separation technologies is improving recovery and operational efficiency.

- Rising demand from electronics and clean energy sectors is boosting the importance of non-ferrous metal recycling.

- Regulatory pressure and environmental policies are encouraging stricter waste management and higher recycling standards across regions.

- Expansion generation and processing infrastructure.

Metal Recycling Market Growth Factors

What Is Driving the Demand for Recycled Metal?

The growing environmental awareness among consumers and industries is pushing the demand for sustainable alternatives to virgin metals. Governments worldwide are implementing regulations and incentives encouraging recycling and waste reduction, which fuels industry adoption. Rising raw material and energy costs have made recycled metals a more cost-effective choice. This dual pressure of ecological responsibility and economic savings is a powerful catalyst for market growth, reshaping how metals are sourced and used sustainably.

How Does Infrastructure Development Impact Metal Recycling?

Rapid urbanization and expanding infrastructure projects are generating increased demand for metals like steel and aluminium, which is turn boosts recycling activities. As construction and manufacturing grow, the use of recycled metals becomes more attractive due to lower costs and environmental benefits. Industries reliant on metals prefer recycled sources to meet sustainability goals and reduce landfill waste. This trend supports a circular economy here scrap metals are continuously reused, promoting resource efficiency amid urban growth. The focus on sustainable building practices further integrates recycling into infrastructure development strategies.

Market Opportunity

Can Recycled Metal Power the Electric Future?

The rapid shift toward electric vehicles and battery storage is pushing manufacturers to secure responsible metal sources. Automakers are now turning to recycled aluminium, copper, and nickel to meet sustainability commitments without relying solely on mining. Major EV producers have publicly stated targets to increase recycled metal content in car bodies, wiring, and battery casing. This creates fresh partnerships between recycles and vehicle manufacturers that were previously disconnected industries. As clean transport accelerates, metal recyclers are becoming suppliers rather than waste processors.

Will Urban Mining Replace Traditional Digging?

Cities are becoming rich reservation of discarded appliances, cables, and industrial scrap that contain high value metals. Instead of extracting minerals from the ground, recyclers are setting up localized hubs to extract them directly from old building and infrastructure. This strategy reduces dependence on politically sensitive mining regions and cuts transportation emissions. Governments are increasingly supporting urban recovery projects to reclaim metals from demolition and renovation sites. As aging cities upgrade their infrastructure, recyclers gain access to a constant flow of premium scrap.

Limitations In The Metal Recycling Market

- Contamination in scrap streams reduces the purity and quality to recycled metals, making it harder to achieve grade specifications required by industrial users.

- High capital and energy requirements for processing and refining metal creates barriers for smaller recyclers and limit expansion in less developed regions.

Metal Recycling Market Segmentation

Metal Type Insights

Why Are Ferrous Metals Segment Dominated the Metal Recycling Market?

Ferrous metals segment dominated the market in 2024. This dominance is attributed to their widespread use across structural, automotive, and industrial applications where material strength and durability are prioritized. The recycling process for ferrous metal is mature and well-integrated into manufacturing loops, allowing them to flow smoothly between scrapyards, processors, and end users. Strong availability of discarded machinery. Building components, and transportation equipment continues to supply a steady stream of reusable ferrous material. Industries increasingly prefer ferrous scrap over virgin extraction authority across the recycling ecosystem.

Non-ferrous metal segment is set to experience the fastest rate of market growth from 2025 to 2034. This growth is mainly fuelled by rising demand for lightweight, corrosion-resistant, and high conductivity materials across sectors like electronics, renewable systems, and transportation. Recyclers are investing heavily in advanced separation technologies to capture aluminium, copper, and specialty alloys more efficiently, unlocking higher value recovery. Growing emphasis on low carbon sourcing is pushing manufacturers to replace primary metals with recycled alternatives wherever possible. As technology improves and collection networks expand, non-ferrous materials are poised to move from a supporting role to a major growth driver.

Scrap Source Insights

What Keeps Industrial Scrap Segment In Command In Metal Recycling Market?

Industrial scrap segment dominated the market in 2024. Its dominance stems from controlled and consistent scrap generation from factories, fabrication plants, and large scale production facilities, which supply cleaner and more uniform material compared to household or municipal sources. Industrial scrap often requires less pre-processing, making it more attractive to recycling companies fosters direct collection agreements and stable supply contracts. This structured ecosystem ensures that industrial scrap remains the preferred source for large metal recovery operations.

Obsolete scrap segment is predicted to witness rapid growth in the market over the forecast period. This surge is driven by rising disposable of outdates appliances, vehicles, and infrastructure materials as modernisation and replacement cycles accelerate. Urban mining initiatives are turning landfills and demolition sites into valuable recovery hubs, allowing recyclers to extract metals from previously ignored waste streams. Public awareness campaigns are also encouraging consumers and businesses to return unused hardware instead of dumping it. As collection programs scale up, obsolete scrap is transforming from disposable problem into a lucrative resource base.

Processing Method Insights

Why Does Melting And Refining Segment Dominated The Metal Recycling Market?

Melting and refining segment maintained a leading position in the market in 2024. This method remains favoured due to its ability to convert scrap into high purity secondary metal that can directly replace virgin material in manufacturing. Established smelters operate with optimized furnaces and energy recovery systems, making mass processing both economical and environmentally favourable. Industries that demand consistent quality standards rely on refined output to meet specification requirements. With decades of infrastructure already in place, melting and refining continue to anchor the processing landscape.

Sorting and shredding segment is set to experience the fastest rate of the market growth from 2025 to 2034. This growth is propelled by automation technologies such as AI scanners, magnetic separators, and high precision density sorting machines that increase throughput while reducing contamination. These advancements allow recyclers to recover more types of metal from mixed waste streams that were previously difficult to process. Faster pre-processing also improves efficient for downstream smelters, creating a smoother recycling chain. As facilities upgrade, sorting and shredding are evolving from basic preparation steps into core value adding operations.

End Use Industry Insights

Why Do Contraction And Infrastructure Dominated The Metal Recycling Market?

construction and Infrastructure segment captured a large portion of the market in 2024. The sector consumers vast quantities of steel, aluminium, and other structural metals, making recycled material an ideal fit for cost reduction and sustainability targets. Governments and developers now prioritize green building standards, which encourage the use of reclaimed components and reprocessed metals. Demolition and renovation projects also supply abundant scrap, creating a natural cycle between removal and reuse. With both supply and demand aligned, construction remains the powerhouse of recycled metal absorption.

The automotive segment is projected to expand rapidly in the market the coming years. Automakers are redesigning vehicles with higher recycled content in frames, wiring, and internal systems to lower environmental footprints. Electrification trends also boost demand for recycled copper, aluminium, and specialty alloys used in batteries and motor components. Collaboration between can manufacturers and recycling networks is becoming more formalized, turning end of life vehicles into structured recovery assets. As sustainability becomes a core manufacturing requirement rather than a marketing claim, automotive applications are becoming central to market expansion.

Regional Insights

What Makes Asia Pacific The Dominant Region In Metal Recycling Market?

The Asia Pacific metal recycling market size is estimated at USD 265.51 billion in 2025 and is anticipated to reach USD 482.64 billion by 2034, growing at a CAGR of 6.86% from 2025 to 2034. Asia Pacific dominated the market in 2024.

Asia Pacific holds the dominant position in the metal recycling market in 2024, driven by rapid industrialization, urbanization, and environmental regulations that promote sustainable practices. The region has a strong manufacturing base producing a large volume of metals, which supports the availability of scrap for recycling. Additionally, the economic benefits of recycling such as energy conservation and cost savings align well with regional growth strategies. Governments in Asia Pacific actively encourage recycling through policies and incentives aimed at reducing reliance on imported raw materials and minimizing environmental degradation. This combination of factors sustains Asia Pacific’s leading role in the global metal recycling industry.

China and India are the forefront of metal recycling growth in the Asia Pacific region, fuelled by their vast industrial bases and stringent environmental laws. China, as the world’s largest steel producer, recycles a significant portion of its scrap metal to supply its manufacturing sector, supported by advanced recycling to meet growing demand from its construction and automotive industries, while aiming to reduce carbon emissions. Both countries benefit from large scale infrastructure projects and expanding urban populations, which generate substantial scrap metal resources. Their leadership is instrumental is shaping the region’s continued dominance in the metal recycling market.

Why Is North America The Fastest Growing Region In Metal Recycling ?

The U.S. metal recycling market size is calculated at USD 87.91 billion in 2024, grew to USD 90.76 billion in 2025, and is projected to reach around USD 121.04 billion by 2034. The market is expanding at a CAGR of 3.25% between 2025 and 2034.

North America is experiencing the fastest growth in the metal recycling market during the forecast period, driven by strong government policies supporting clean energy and sustainability goals. The region is focused on replacing primary metals with secondary recycled metals in industries such as automotive, construction, and consumer goods. Increased investment in advanced recycling technologies, including AI based sorting and automation, enhance recovery efficiency and reduce environmental impact. Growing infrastructure development and industrial expansion further boost demand for recycled metals. This combination of regulatory support, technological innovation, and industrial growth peoples the robust market expansion in North America.

The United States stands out as the dominant country in North America’s metal recycling market, with a well-established infrastructure and substantial manufacturing base demanding recycled metals. The U.S. benefits from government incentives promoting green initiates and steelmaking electrification, which increase the adoption of recycled materials. Regions like the Southwest and West U.S. notably contribute to growth through urban expansion and strict environmental regulations, respectively. The presence of leading recycling companies and continuous technological advancements further strengthen the U.S. position. This dominance shapes North America’s competitive landscape and drives the continued rise of the metal recycling industry in the region.

More Insights in Towards Chemical and Materials:

- Copper Foil Market : The global copper foil market volume is calculated at 387.50 kilo tons in 2024, grew to USD 415.07 kilo tons in 2025 and is predicted to hit around 770.50 kilo tons by 2034, expanding at healthy CAGR of 7.11% between 2025 and 2034.

- Copper Wire Market : The global copper wire market size accounted for USD 159.25 billion in 2025 and is forecasted to hit around USD 284.27 billion by 2034, representing a CAGR of 6.65% from 2025 to 2034.

- Aluminium Oxide Market : The global aluminum oxide market volume was reached at 160.12 million tons in 2024 and is expected to be worth around 215.45 million tons by 2034, growing at a compound annual growth rate (CAGR) of 3.01% over the forecast period from 2025 to 2034.

- Aluminum Trihydrate (ATH) Market : The global aluminum trihydrate (ATH) market volume was reached at 2850.21 kilo tons in 2024 and is expected to be worth around 4653.45 kilo tons by 2034, growing at a compound annual growth rate (CAGR) of 5.02% over the forecast period 2025 to 2034.

- Aluminum Foil Market : The global aluminum foil market size was reached at USD 29.33 billion in 2024 and is expected to be worth around USD 48.46 billion by 2034, growing at a compound annual growth rate (CAGR) of 5.15% over the forecast period 2025 to 2034.

- Aluminum Composite Materials Market : The global aluminum composite materials market size is calculated at USD 3.84 billion in 2024, grew to USD 4.14 billion in 2025, and is projected to reach around USD 8.18 billion by 2034. The market is expanding at a CAGR of 7.85% between 2025 and 2034.

- Metal-Organic Frameworks Market : The global metal-organic frameworks market volume was reached at 55,000.0 tons in 2024 and is expected to be worth around 3,43,966.3 tons by 2034, growing at a compound annual growth rate (CAGR) of 20.12% over the forecast period 2025 to 2034.

- Metal Carboxylates Market : The global metal carboxylates market size accounted for USD 6.55 billion in 2025 and is forecasted to hit around USD 10.83 billion by 2034, representing a CAGR of 5.75% from 2025 to 2034.

- Metal Casting Market : The global metal casting market size was reached at USD 152.47 billion in 2024 and is estimated to surpass around USD 262.91 billion by 2034, growing at a compound annual growth rate (CAGR) of 5.60% during the forecast period 2025 to 2034.

- Asia Pacific Metal Casting Market : The Asia Pacific metal casting market size was reached at USD 85.67 billion in 2024 and is expected to be worth around USD 142.91 billion by 2034, growing at a compound annual growth rate (CAGR) of 5.25%over the forecast period 2025 to 2034.

Metal Recycling Market Top Key Companies:

- European Metal Recycling

- CMC

- GFG Alliance

- Norsk Hydro ASA

- Kimmel Scrap Iron & Metal Co., Inc.

- Schnitzer Steel Industries, Inc.

- Novelis

- Tata Steel

- Sims Metal

- Utah Metal Works

Recent Developments

- In March 2025, in a significant move within the U.S. metal recycling sector, Toyota Tsusho America has completed the acquisition of Radius Recycling for $1.34 billion. This strategic acquisition aims to bolster Toyota Tsusho’s presence in the U.S. market and enhance its recycling capabilities, particularly in the automotive sector. The deal is expected to facilitate the expansion of Radius Recycling’s operations and contribute to the growth of sustainable metal recycling practices in the region.

- In September 2025, the metal recycling industry is evolving with innovative green steel production technologies in the United States. start-ups like Boston Metal utilize electricity to produce steel with substantially lower carbon emissions compared to traditional blast furnaces. This shift supports sustainability while maintaining production capacities, although scaling remains challenging. Such developments exemplified the potential for more environmentally friendly metal recycling and steelmaking, aligning industry growth with climate goals.

Metal Recycling Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2019 to 2034. For this study, Towards Chemical and Materials has segmented the global Metal Recycling Market

By Metal Type

- Ferrous Metals (steel, iron)

- Non-Ferrous Metals

- Aluminum

- Copper

- Lead

- Nickel

- Zinc

- Others

By Scrap Source

- Industrial Scrap

- Obsolete Scrap (end-of-life products, vehicles, appliances)

- Construction & Demolition Scrap

By Processing Method

- Collection & Sorting

- Shredding

- Melting & Refining

- Others (baling, shearing, briquetting)

By End-Use Industry

- Construction & Infrastructure

- Automotive

- Electronics & Electricals

- Packaging

- Machinery & Equipment

- Shipbuilding

- Others

By Regional

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/price/5830

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Automotive | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: sales@towardschemandmaterials.com

Web: https://www.towardschemandmaterials.com/

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.